Deep Hedging of Green PPAs

[1]:

import datetime as dt

import sys

sys.path.insert(0,'../..')

from typing import List

import numpy as np

import matplotlib.pyplot as plt

import json

import os

os.environ["CUDA_VISIBLE_DEVICES"] = "-1"

from rivapy.tools.datetime_grid import DateTimeGrid

from rivapy.models.residual_demand_fwd_model import WindPowerForecastModel, MultiRegionWindForecastModel, ResidualDemandForwardModel, LinearDemandForwardModel

from rivapy.instruments.ppa_specification import GreenPPASpecification

from rivapy.models.residual_demand_model import SmoothstepSupplyCurve

from rivapy.models import OrnsteinUhlenbeck

from rivapy.pricing.green_ppa_pricing import GreenPPADeepHedgingPricer, DeepHedgeModel

import numpy as np

from scipy.special import comb

from IPython.display import display, HTML

display(HTML("<style>.container { width:80% !important; }</style>"))

%load_ext autoreload

%autoreload 2

%matplotlib inline

/home/doeltz/doeltz/development/RiVaPy/rivapy/__init__.py:11: UserWarning: The pyvacon module is not available. You may not use all functionality without this module. Consider installing pyvacon.

warnings.warn('The pyvacon module is not available. You may not use all functionality without this module. Consider installing pyvacon.')

2023-06-22 17:57:18.177259: W tensorflow/stream_executor/platform/default/dso_loader.cc:64] Could not load dynamic library 'libcudart.so.11.0'; dlerror: libcudart.so.11.0: cannot open shared object file: No such file or directory

2023-06-22 17:57:18.177279: I tensorflow/stream_executor/cuda/cudart_stub.cc:29] Ignore above cudart dlerror if you do not have a GPU set up on your machine.

Residual Demand Forward Model

[2]:

days = 10

timegrid = np.linspace(0.0, days*1.0/365.0, days*24)

forward_expiries = [timegrid[-1]]

[3]:

wind_onshore = WindPowerForecastModel(region='Onshore', speed_of_mean_reversion=0.1, volatility=4.80)

wind_offshore = WindPowerForecastModel(region='Offshore', speed_of_mean_reversion=0.5, volatility=4.80)

regions = [ MultiRegionWindForecastModel.Region(

wind_onshore,

capacity=1000.0,

rnd_weights=[0.8,0.2]

),

MultiRegionWindForecastModel.Region(

wind_offshore,

capacity=100.0,

rnd_weights=[0.2,0.8]

)

]

wind = MultiRegionWindForecastModel('Wind_Germany', regions)

model = LinearDemandForwardModel(wind_power_forecast=wind, x_volatility=1.4 , x_mean_reversion_speed=2.0,

power_name= 'Power_Germany')

[5]:

np.random.seed(42)

rnd = np.random.normal(size=model.rnd_shape(n_sims=10_000, n_timesteps=timegrid.shape[0]))

model_result = model.simulate(timegrid, rnd, expiries=forward_expiries,

initial_forecasts={'Onshore': [0.8],

'Offshore': [0.6]},

power_fwd_prices = [100])

[6]:

model_result.keys()

[6]:

{'Offshore_FWD0', 'Onshore_FWD0', 'Power_Germany_FWD0', 'Wind_Germany_FWD0'}

PPA Hedging

[7]:

class Repo:

def __init__(self, repo_dir):

self.repo_dir = repo_dir

self.results = {}

with open(repo_dir+'/hedge_results.json','r') as f:

self.results = json.load(f)

def run_hedge_experiment(self, val_date, ppa_spec, model, **kwargs):

params = {}

params['ppa_spec'] = ppa_spec.to_dict()

params['ppa_spec_hash'] = ppa_spec.hash()

params['model'] = model.to_dict()

params['model_hash'] = model.hash()

params['pricing_param'] = kwargs

hash_key = FactoryObject.hash_for_dict(params)

#if hash_key in results:

pricing_result = GreenPPADeepHedgingPricer.price(val_date,

ppa_spec,

model,

**kwargs)

return pricing_results

from rivapy.tools.interfaces import FactoryObject

def compute_pnl_figures(pricing_results):

pnl = pricing_results.hedge_model.compute_pnl(pricing_results.paths, pricing_results.payoff)

return {'mean': pnl.mean(), 'var': pnl.var(), '1%':np.percentile(pnl,1), '99%': np.percentile(pnl,1)}

def compute_pnl(pricing_results):

return pricing_results.hedge_model.compute_pnl(pricing_results.paths, pricing_results.payoff)

[8]:

val_date = dt.datetime(2023,1,1)

strike = 0.3 #0.22

spec = GreenPPASpecification(udl='Power_Germany',

technology = 'Wind',

location = 'Onshore',

schedule = [val_date + dt.timedelta(days=2)],

fixed_price=strike,

max_capacity = 1.0)

[9]:

pricing_result = GreenPPADeepHedgingPricer.price(val_date,

spec,

model,

model,

initial_forecasts={'Onshore': [0.8, 0.7,0.6,0.5],

'Offshore': [0.6,0.6,0.6,0.6]},

power_fwd_prices=[1.0],

forecast_hours=[10, 14, 18],

additional_states=['Offshore'],

depth=3, nb_neurons=32, n_sims=100_000,

regularization=0.0,

epochs=20, verbose=1,

tensorboard_logdir = 'logs/' + dt.datetime.now().strftime("%Y%m%dT%H%M%S"),

initial_lr=5e-4,

decay_steps=8_000,

batch_size=100, decay_rate=0.8, seed=42)

---------------------------------------------------------------------------

TypeError Traceback (most recent call last)

/tmp/ipykernel_437888/2057733429.py in <module>

----> 1 pricing_result = GreenPPADeepHedgingPricer.price(val_date,

2 spec,

3 model,

4 model,

5 initial_forecasts={'Onshore': [0.8, 0.7,0.6,0.5],

TypeError: price() got multiple values for argument 'initial_forecasts'

[11]:

model = DeepHedgeModel.load('depp')

WARNING:tensorflow:No training configuration found in save file, so the model was *not* compiled. Compile it manually.

WARNING:tensorflow:No training configuration found in save file, so the model was *not* compiled. Compile it manually.

[37]:

pricing_results = run_hedge_experiment(val_date,

spec,

model,

initial_forecasts={'Onshore': [0.8, 0.7,0.6,0.5],

'Offshore': [0.6,0.6,0.6,0.6]},

power_fwd_prices=[1.0],

forecast_hours=[10, 14, 18],

additional_states=['Offshore'],

depth=3, nb_neurons=32, n_sims=100_000,

regularization=0.0,

epochs=20, verbose=1,

tensorboard_logdir = 'logs/' + dt.datetime.now().strftime("%Y%m%dT%H%M%S"),

initial_lr=5e-4,

decay_steps=8_000,

batch_size=100, decay_rate=0.8, seed=42)

/home/doeltz/doeltz/development/RiVaPy/rivapy/tools/datetime_grid.py:24: FutureWarning: Argument `closed` is deprecated in favor of `inclusive`.

self.dates = pd.date_range(start, end, freq=freq, tz=tz, closed=closed).to_pydatetime()

Epoch 1/20

1000/1000 [==============================] - 7s 2ms/step - loss: 1.0018e-04

Epoch 2/20

1000/1000 [==============================] - 2s 2ms/step - loss: 7.8207e-05

Epoch 3/20

1000/1000 [==============================] - 2s 2ms/step - loss: 7.9591e-05

Epoch 4/20

1000/1000 [==============================] - 2s 2ms/step - loss: 7.8396e-05

Epoch 5/20

1000/1000 [==============================] - 2s 2ms/step - loss: 7.7541e-05

Epoch 6/20

1000/1000 [==============================] - 2s 2ms/step - loss: 7.6689e-05

Epoch 7/20

1000/1000 [==============================] - 2s 2ms/step - loss: 7.5947e-05

Epoch 8/20

1000/1000 [==============================] - 2s 2ms/step - loss: 7.6003e-05

Epoch 9/20

1000/1000 [==============================] - 2s 2ms/step - loss: 7.4701e-05

Epoch 10/20

1000/1000 [==============================] - 2s 2ms/step - loss: 7.4335e-05

Epoch 11/20

1000/1000 [==============================] - 2s 2ms/step - loss: 7.4303e-05

Epoch 12/20

1000/1000 [==============================] - 2s 2ms/step - loss: 7.3094e-05

Epoch 13/20

1000/1000 [==============================] - 2s 2ms/step - loss: 7.3400e-05

Epoch 14/20

1000/1000 [==============================] - 2s 2ms/step - loss: 7.3353e-05

Epoch 15/20

1000/1000 [==============================] - 2s 2ms/step - loss: 7.3494e-05A: 0s

Epoch 16/20

1000/1000 [==============================] - 2s 2ms/step - loss: 7.3430e-05

Epoch 17/20

1000/1000 [==============================] - 2s 2ms/step - loss: 7.2063e-05

Epoch 18/20

1000/1000 [==============================] - 2s 2ms/step - loss: 7.2050e-05

Epoch 19/20

1000/1000 [==============================] - 2s 2ms/step - loss: 7.2099e-05

Epoch 20/20

1000/1000 [==============================] - 2s 2ms/step - loss: 7.2132e-05

[39]:

pricing_results.paths.keys()

#ttm

[39]:

dict_keys(['Power_Germany_FWD0', 'Onshore_FWD0', 'Offshore_FWD0'])

[85]:

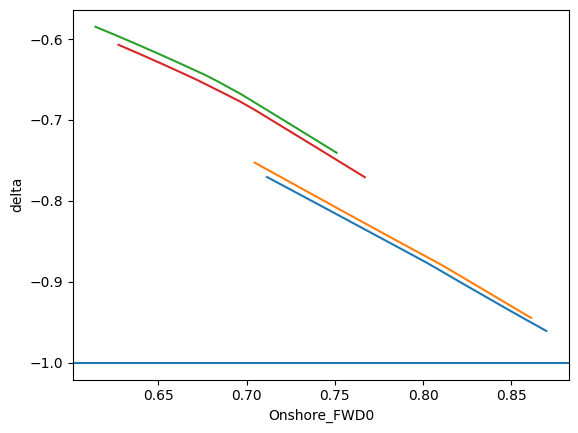

t = 48

p=10.0

projection = np.linspace(0.9,1.1, 250)

projected_key = 'Onshore_FWD0'

for selected in [2,5,100,400]:

#selected = 2

#key = 'Power_Germany_FWD0'

#x = np.percentile(pricing_results.paths[key][-1,:],p)

#selected = np.abs(x-pricing_results.paths[key][-1,:]).argmin()

paths = {}

T = pricing_results.hedge_model.timegrid[-1]

ttm = (T-pricing_results.hedge_model.timegrid[t])/T

for k,v in pricing_results.paths.items():

if k == projected_key:

paths[k] = projection*v[t,selected]

x = projection*v[t,selected]

else:

paths[k] = np.full(shape=(projection.shape[0]), fill_value=v[t,selected])

delta = pricing_results.hedge_model.compute_delta(paths, ttm)

plt.plot(x, delta)

plt.xlabel(projected_key)

plt.axhline(-1.0)

plt.ylabel('delta');

8/8 [==============================] - 0s 3ms/step

8/8 [==============================] - 0s 3ms/step

8/8 [==============================] - 0s 2ms/step

8/8 [==============================] - 0s 1ms/step

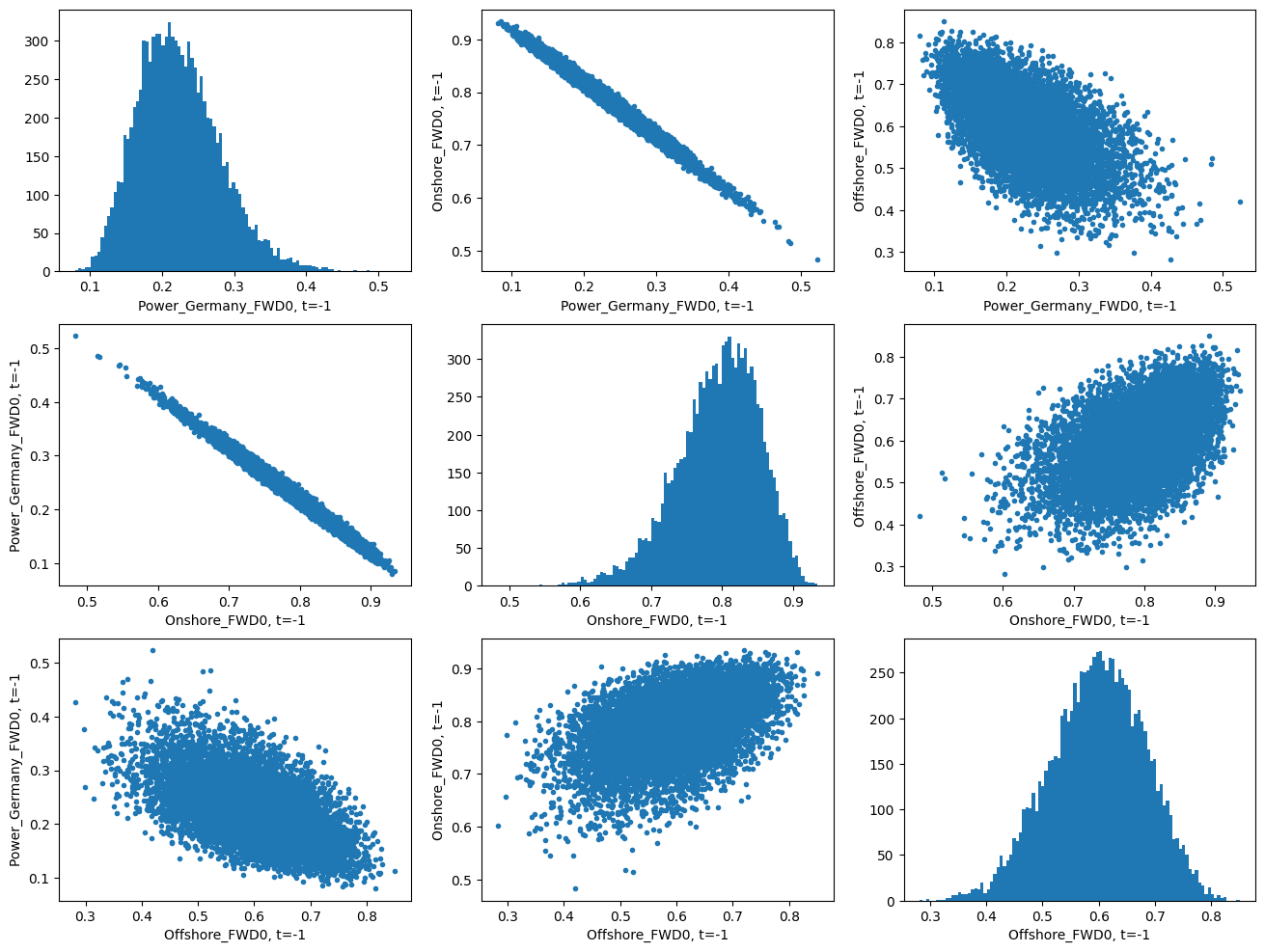

Path Plots

[67]:

t = -1

plt.figure(figsize=(16,12))

n_x = 3

n_y = 3

i=1

for k,v in pricing_results.paths.items():

for l,w in pricing_results.paths.items():

plt.subplot(n_x,n_y,i)

if k==l:

plt.hist(v[t,:], bins=100)

plt.xlabel(k+', t='+str(t))

else:

plt.plot(v[t,:], w[t,:], '.')

plt.xlabel(k+', t='+str(t))

plt.ylabel(l+', t='+str(t))

i += 1

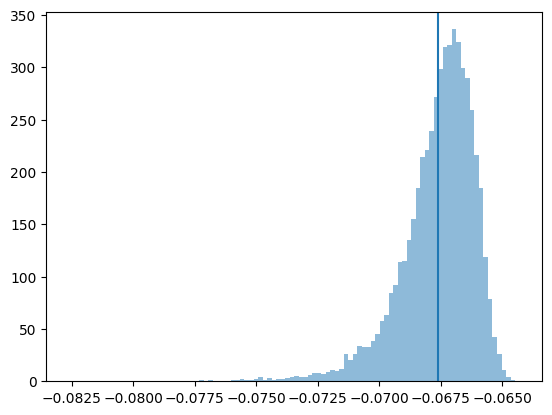

Hedge PnL Distribution

[12]:

pnl = pricing_results.hedge_model.compute_pnl(pricing_results.paths, pricing_results.payoff)

#plt.hist(pricing_results.payoff, bins=100, alpha=0.5, density=True)

plt.axvline(pnl.mean())

plt.hist(pnl,bins=100, alpha=0.5, density=True);

313/313 [==============================] - 8s 4ms/step

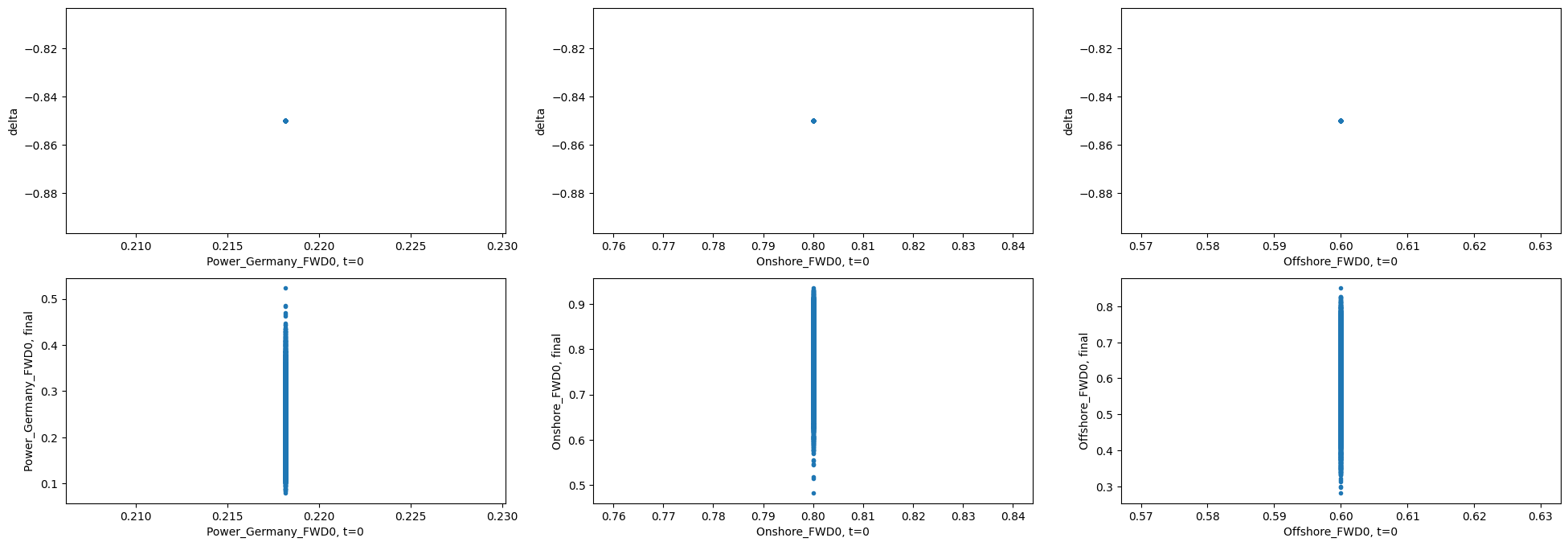

Delta Plots

[64]:

t = 0

n_x = 2

n_y = 3

plt.figure(figsize=(24,8))

delta = pricing_results.hedge_model.compute_delta(pricing_results.paths, t)

i=1

for k,v in pricing_results.paths.items():

plt.subplot(n_x, n_y, i)

plt.plot(v[t,:], delta,'.')

plt.xlabel(k+', t='+str(t))

plt.ylabel('delta')

i+= 1

for k,v in pricing_results.paths.items():

plt.subplot(n_x, n_y, i)

plt.plot(v[t,:], v[-1,:],'.')

plt.xlabel(k+', t='+str(t))

plt.ylabel(k+', final')

i+= 1

313/313 [==============================] - 1s 2ms/step

[ ]: